Research Report

Growth and innovation in the chemical industry

5-minute read

Research Report

5-minute read

It’s an exciting time in the chemical industry. Opportunities abound, with everything from greenhouse gas (GHG) reduction mandates to electric vehicles, 3D printing and changing end-consumer sentiment driving demand for new chemical products.

Meeting that demand means that innovation is more important than ever. The question is, are chemical companies ready for the opportunity? The answer depends on one’s perspective and the timeframes involved. However, it seems clear that the chemical industry is at an inflection point where the need for breakthrough innovation is increasing rapidly—and a “more of the same” approach will not be enough.

To explore this question further and glean new insights for chemical companies, Accenture analyzed investments across the following six key levers related to growth and innovation:

The findings from the analysis point to a need for the industry to move from its traditional approaches to a reimagined focus on delivering breakthrough innovations, quickly and consistently.

Patents

Patent filings fall into three main categories: materials, applications and processes. Of these three, materials-related patents were the most common. Many of these cover incremental improvements of existing materials—rather than new materials—and focus on enhancing performance characteristics such as flexibility, durability, electroluminescence and chemical resistance. Meanwhile, there was a relatively low number of process patents. This may be in part due to a desire not to publicize process innovations, but it also suggests that the industry may not be investing enough in the core processes that will be required to reduce carbon footprints and meet the growing demand for more sustainable products.

Startups

Chemical-related startups, which have seen dramatic growth in funding, are addressing many of the industry’s important growth areas, including building materials, waste management, additive manufacturing and machine learning (ML), which together represent about 30% of the total startup investment in recent years. Nearly 20% of investments have been focused on digital solutions such as AI/ML for molecule discovery and quantum computing for simulations, or activities in the fields of e-commerce and business-to-business interactions. Startups exploring materials that support CO2 reductions and the circular economy account for 10% of investment share.

Corporate venturing

Much of the industry’s corporate venturing continues to focus on existing product groups such as agrichemicals, paints and coatings, and food ingredients. Chemical companies appear to view their corporate venturing activities as an extension of their in-house R&D efforts, rather than a way to explore uncharted territory. And instead of seeking disruptive innovations for the market, they are primarily targeting improvements to their internal capabilities and looking for new applications for existing molecules. The picture changes somewhat with technology-related investments, with growth in AI, 3D printing, hydrogen/fuel cells and analytics—areas where companies presumably see potential for innovation.

Partnerships

While getting close to the customer is a well-established credo in the industry, partnerships with customers have been less frequent than those with other chemical companies on average over the past five years. Looking forward, growing fields such as 3D printing and circular economy products and processes will require close collaboration with customers. Increased partnering with technology providers, currently fairly rare, also offers opportunity. As part of an asset-intensive and data-rich industry, chemical companies can use AI, ML, analytics, Industry X, quantum computing and so forth to further improve operations and extract value from data and assets.

Increase in the number of announced partnerships since 2016, with production being a dominant focus

Partnerships over the past five years that have been between chemical companies, the most common type

Partnerships over the past five years that have been between chemical companies and their customers

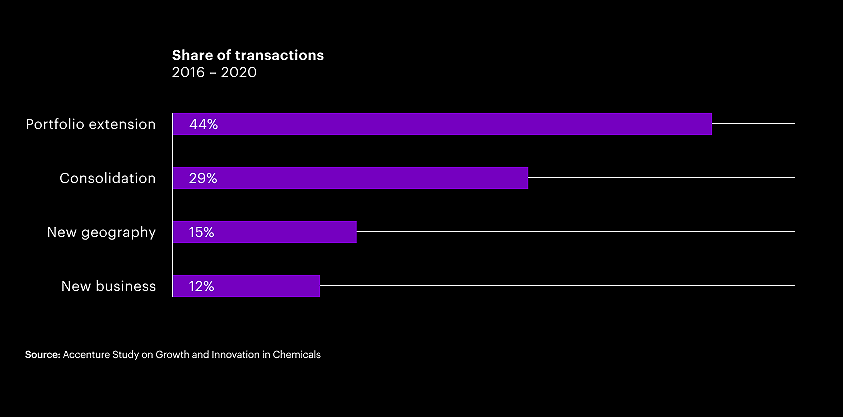

Mergers and acquisitions

The majority of M&A investments have targeted extensions to existing products or additional business in segments already served. Far fewer focused on entry into new markets and moving into new businesses. In terms of products and offerings involved in M&A, the highest growth rates were in chemicals and solutions for electronics, information technology and plastic products. Overall, however, the majority of transactions focused on agrichemicals, “traditional” specialty chemicals, or coatings, adhesives, sealants and inks.

Figure 2: M&A transactions target existing, rather than new, business

Capital projects

Chemical companies have increased their capital investments in newer fields such as batteries, recycling and pyrolysis. However, a majority (68%) of investments are still going into traditional areas such as basic and intermediate chemicals, thermoplastics and fertilizers. Some companies are shifting investments to new segments related to the circular economy and GHG reductions, but the numbers are still fairly small. Overall, the industry may not be pivoting quickly enough to address the requirements of a circular economy.

In the very near future, the need for all industries to reduce greenhouse gases and support a circular economy will require a massive wave of innovation from chemical companies.

On the one hand, the chemical industry has well-established innovation capabilities and is pursuing a range of innovations—that is, the glass is half full. On the other hand, it tends to focus on improving today’s offerings, rather than creating new ones. In a rapidly changing, competitive world where digital- and sustainability-related transformation is a requirement for success, that traditional approach will not be enough—that is, the glass is half empty.

If chemical companies fall behind in the race to deliver more innovation on more fronts, they may miss tomorrow’s major growth opportunities. They run the risk of finding themselves disrupted by a growing number of chemical-related startups that are essentially filling the gaps left open by the industry’s more traditional approach to innovation.

The chemical industry will need to make fundamental changes to the way it drives innovation. And assessing investments across the six levers defined above is an essential first step. It is clear that tremendous opportunity lies ahead—but future growth will require companies to deliver a broad and evolving range of innovative new products, processes and services.

Short on time? Read the executive summary of our report that explores six key levers of growth and innovation in the chemical industry.

View the executive summary

The Accenture Study on Growth and Innovation in Chemicals defined and analyzed the innovation lifecycle in the chemical industry across six key levers: patents, startups, corporate venturing, partnerships, mergers and acquisitions, and capital projects. For each lever, clusters of primary data were created, and traditional as well as advanced analytics were applied to extract insights. The research encompassed the following: