RESEARCH REPORT

The changing face of M&A in the chemical industry

5-minute read

RESEARCH REPORT

5-minute read

Every year, the chemical industry sees hundreds of mergers and acquisitions (M&A) around the globe. Altogether, this activity means that about 20% of industry revenue has changed ownership over the course of a decade—and M&A is now an important tool for change in the sector.

Traditional M&A drivers, such as consolidation and portfolio extension, are still important, according to the Accenture Chemical Industry M&A Study, a recent analysis of M&A transactions over the last 10 years. But the nature of M&A is evolving. As chemical companies look for ways to contend with ongoing uncertainty and move to a more sustainable future, M&A is often a source of growth and innovation as they seek to optimize their portfolios, adopt new business models and reshape themselves to thrive in the coming years.

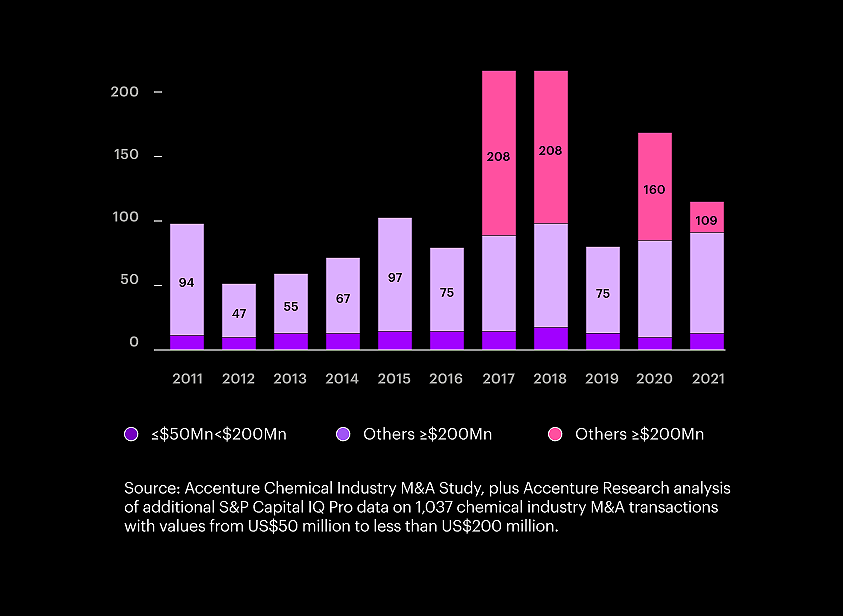

In recent years, the chemical industry has seen several exceptionally large transactions and waves of consolidation. But beneath these high-profile spikes in activity lies a steady level of M&A that has continued, even through global economic slowdowns. (See Figure 1)

Figure 1: Completed chemical industry M&A transactions, 2011–2021

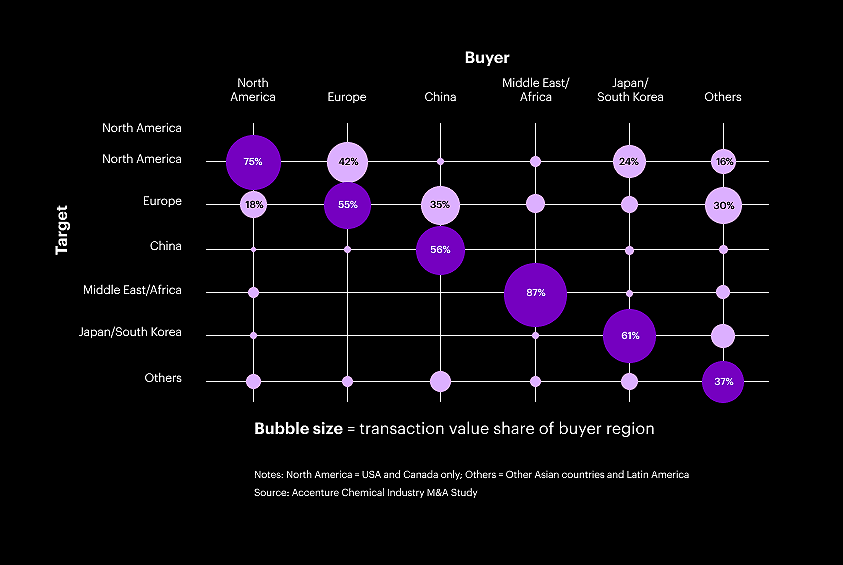

In terms of geographic preferences, most chemical industry M&A deals take place within companies’ home regions. That is, in terms of transaction value, deals are most prevalent where North American buyers have targeted North American companies; the same holds true between European buyers and targets, and so on. But there is some notable inter-regional activity, particularly involving Europe and Asia. (See Figure 2)

Figure 2: Regional preferences in M&A

The rationales of both buyers and sellers in M&A were also explored. For buyers, the top two drivers were consolidation and portfolio extension—an indication that chemical companies are fairly risk-averse in their approach to M&A, as they focus largely on what they already know rather than looking to diversify into entirely new areas. Specifically for buyers, the research revealed:

are motivated by a desire to consolidate.

are looking to extend their portfolios.

are pursuing investment opportunities.

are expanding with forward or backward integration.

Turning to the M&A rationale for sellers, they cited a range of reasons for their actions. To name a few, more than half the transactions involved the sale of a whole company, with “investor exits” and “synergies” being the most common motives. About one-fifth of the transactions involved the sale of a segment of the business to refocus the portfolio, or because the segment was underperforming or encountering financial or antitrust issues.

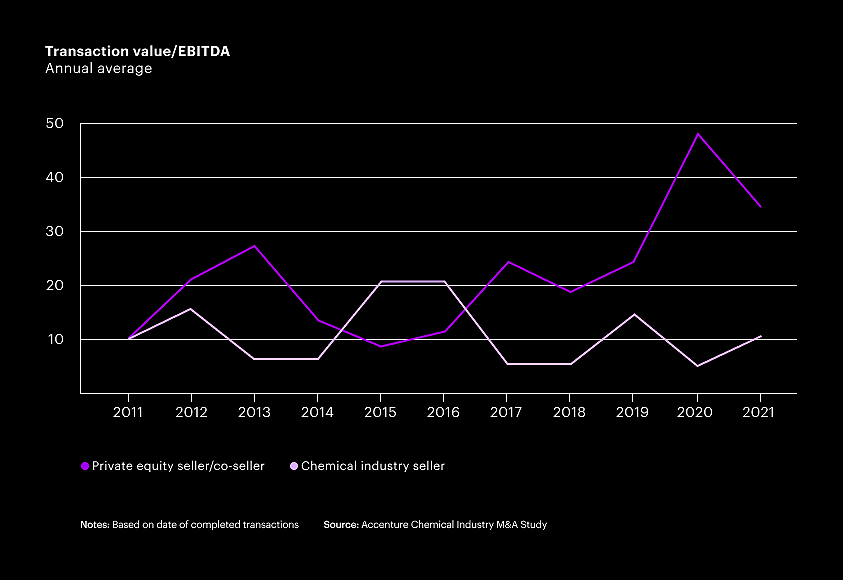

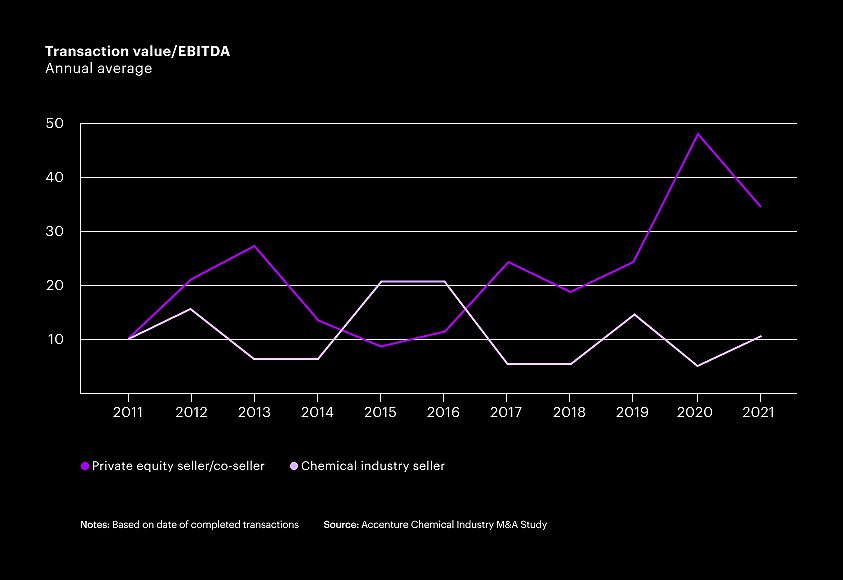

Private equity is playing an increasingly prominent role in the M&A arena. In the last 10 years, it has executed between US$16 billion and US$23 billion in transactions each year in the chemical industry, accounting for 23% of total transaction value on average over the entire period.

Proving to be highly effective players in the industry, private equity groups frequently buy assets from chemical companies, increase their value over a few years and sell them for substantially more. And quite often, these groups will sell at higher multiples compared to chemical company sellers. (See Figure 3) This suggests that chemical companies may be missing out on higher multiples because they are foregoing opportunities to restructure and optimize businesses before selling them.

Figure 3: Private equity vs. chemical company multiples in M&A

Meanwhile, greenhouse gas (GHG) emissions reductions—a major issue in the industry—appear to be emerging as an important factor in M&A decisions. This is not surprising since chemical companies will have to make significant capital investments in GHG-intensive assets in order to meet net-zero goals.

The research identified a pattern in which companies are selling businesses that produce both higher levels of GHG emissions and relatively lower financial returns. For example, one company divested a large fertilizer business that contributed 50% to its GHG emissions but only 5% to its EBITDA; another divested a synthetic rubber business responsible for 25% of the company’s emissions and just 9% of EBITDA. While GHG considerations may not be the sole driver of these divestment activities, they appear to be having a growing influence on M&A-related decisions.

For chemical companies, understanding how to approach M&A will be key to successful, value-creating transactions. There are five imperatives to consider in shaping that approach:

In the coming years, M&A is likely to remain a familiar part of the chemical industry. And its growing role as a powerful tool for change means that companies that enhance and expand their M&A capabilities will be in better position to innovate, compete and grow as the industry evolves.

The Accenture Chemical Industry M&A Study examined mergers, acquisitions and divestments from 2011–2021. Global in scope, the study encompassed transactions of US$200 million or more. This totaled 760 deals with a collective value of US$1.1 trillion, representing 91% of the total transaction value in the industry during this 10-year period. The study was based on an analysis of data from the S&P Capital IQ Pro market-intelligence platform and press announcements from Dow Jones Factiva.